Save 15% on Solar with the Clean Electricity Investment Tax Credit (CE ITC)

A federal program now gives certain tax-exempt organizations a significant way to save on solar energy projects. The Clean Electricity Investment Tax Credit (CE ITC) was introduced in the 2025 Federal Budget and formally passed into law as part of Bill C-15 (the Budget 2025 Implementation Act, No. 1). This program is designed to make solar and other clean electricity projects more accessible for organizations that do not pay corporate income taxes — including municipalities, Crown corporations, and Indigenous governments.

For these organizations, which were historically unable to benefit from federal tax credits, this change is significant. The CE ITC helps eliminate one of the largest barriers to solar adoption: high upfront costs. When paired with programs like Ontario’s Save on Energy incentives, it creates a strong financial case for moving forward with solar.

This article outlines what the CE ITC is, who it supports, and why Bill C-15 marks a major milestone for clean energy investment in Canada.

NOTE: This article will be updated as new information regarding the CE ITC is finalized. (Last updated April 16, 2026)

What is the Clean Electricity Investment Tax Credit (CE ITC)?

The CE ITC is a federal refundable tax credit under section 127.491 of the Income Tax Act that supports investments in solar and other clean electricity infrastructure. It was formally enacted by Bill C-15 (Budget 2025 Implementation Act, No. 1), giving eligible organizations the certainty they need to begin planning and moving forward with clean energy projects.

The CE ITC is similar in concept to the existing Clean Technology Investment Tax Credit (CT ITC), but it is specifically designed to reach organizations that do not pay corporate income taxes — entities that own much of Canada’s electricity generation infrastructure but were previously excluded from federal clean energy incentives.

Who Benefits from the CE ITC?

The CE ITC is designed for organizations that do not pay corporate income tax but that own or invest in electricity generation assets. Eligible entities under the legislation include:

Municipal governments and municipal corporations

Designated provincial Crown corporations (90%+ Crown-owned)

Corporations 90%+ owned by municipalities or Indigenous governments

Indigenous communities and Indigenous government corporations

Pension investment corporations and qualifying pension trusts

Taxable Canadian corporations (which may also access the CT ITC)

It is important to note that registered charities and non-profit organizations are not included in the CE ITC’s eligible entity list. The program was designed specifically for entities that own large-scale electricity generation infrastructure, such as Crown utilities and municipal power corporations. Organizations in the charitable and non-profit sector should speak with an advisor about other available options for accessing federal clean energy incentives.

For eligible organizations, the CE ITC levels the playing field by offering a direct cash rebate, making projects feasible that may have previously been delayed or cancelled due to high upfront costs.

How the CE ITC Works

Eligible organizations can receive 15% of eligible project costs back as a refundable credit, effectively reducing the capital required to build solar or clean electricity systems. For tax-exempt entities such as municipalities and Crown corporations, the credit is paid directly as a refund — even though these organizations have no tax payable.

The CE ITC applies to property that became available for use on or after April 16, 2024, and runs through December 31, 2034. This means organizations that have already invested in eligible clean electricity projects since April 2024 may be able to benefit retroactively.

The CE ITC can also be combined with other grants and incentive programs, such as Ontario’s Save On Energy grant for load displacement solar. By reducing upfront costs, the credit improves project returns and makes planning solar installations more straightforward for eligible organizations.

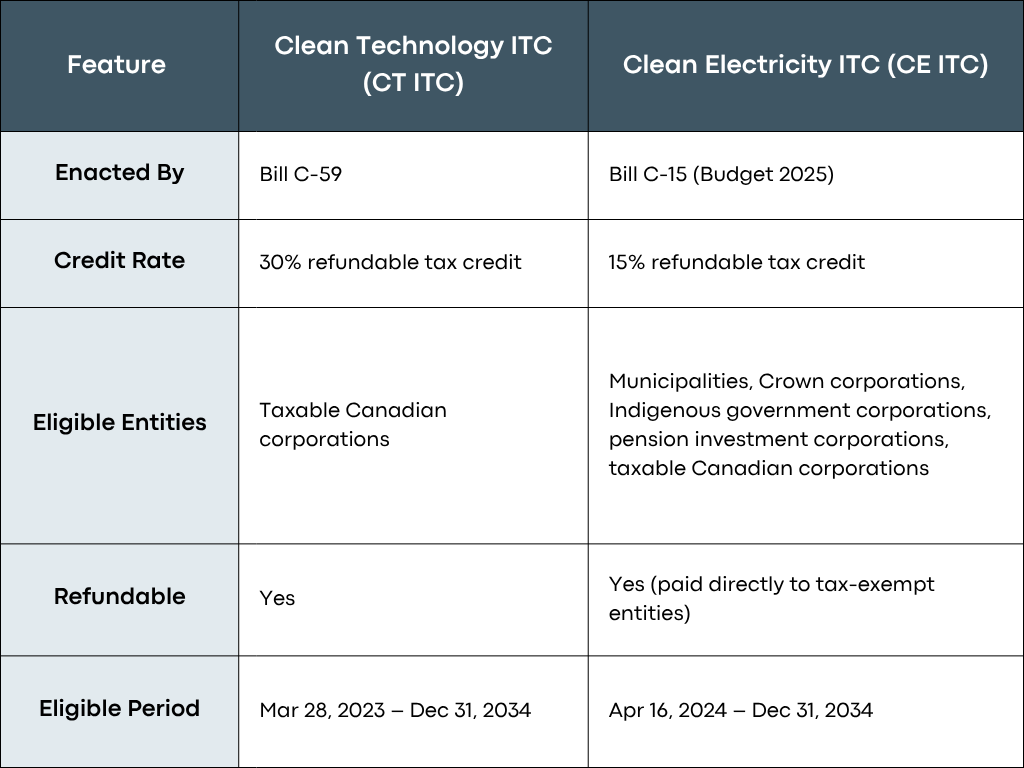

How Does the CE ITC Compare to the CT ITC?

The CE ITC does not replace the CT ITC — the two programs serve different groups. Here is a simplified comparison:

How VCT Group Helps You Maximize Your CE ITC Savings

VCT Group helps eligible organizations navigate the CE ITC and other available incentive programs to make solar projects practical and cost-effective. Our team guides you through the planning process, showing how the credit applies to your project and how it can be combined with other grants to maximize savings. We also handle all necessary documentation and compliance requirements, making the process straightforward for your organization.

By working with VCT Group, your organization can reduce upfront costs, improve project returns, and bring clean electricity projects to life. If your organization is a municipality, Crown corporation, Indigenous community, or other eligible entity considering solar, now is an ideal time to start planning.

Are you ready to explore solar for your organization? Contact VCT Group today to see how the CE ITC can help make solar projects achievable and affordable.